Many terms and phrases that appear in the Insolvency & Bankruptcy Code 2016 require a thorough examination to understand them in their entirety. One such term is an ‘Associate Company’. A section of the code where this phrase matters immensely is Section 29A which lays down the ineligibility criteria for resolution applications. In this article, we take a closer look at the definition of Associate Company.

Albeit a critical concept, the phrase ‘Associated Company’ is not explicitly defined under IBC 2016. However, Section 3(37) of the code states that the words or expressions that are not defined under the code can carry the meaning or interpretations assigned to such words or expressions in any of the following acts namely – Indian Contracts Act, 1872, the SEBI Act, 1992, the Securities Contract (Regulation) Act, 1956, the Recovery of Debts due to Financial banks and Institutions Act, 1993, the Limited Liability Partnership Act, 2008, and the Companies Act, 2013. Therefore, let’s start by looking at the definition provided for this term under the Companies Act 2013.

Definition of Associate Company:

As per Section2(6) of the Companies Act, 2013, an “associate company (A)”, in relation to another company (B), refers to a company in which that other company (B) has a significant influence, but which is not a subsidiary company of the company having such influence. The associated company, however, can refer to a joint venture company.

Further, significant influence is defined in the Act as:

As per Section 2(27) of the Companies Act, 2013, the word “control” shall include the right to appoint a majority of the directors or to control the management or policy decisions exercisable by a person or persons acting individually or in concert, directly or indirectly, including by virtue of their shareholding or management rights or shareholders agreements or voting agreements or in any other manner;

Meaning, if an entity/person owns more than 20% of the total share capital of say ‘Company A’, or if an entity or a person has the right to appoint a majority of the directors in Company A through any agreement (shareholders agreement or others) or if there exists any agreement that allows the entity/person to control key decisions of Company A, then such entity/person is considered an associated party/asscociate company to the Company A.

The Indian Accounting Standards (IAS 28) also defines an associate company as a company where an investor has significant influence. Significant Influence is further defined in IAS 28 as ‘the power to participate in the financial and operating policy decisions of the company but not control or jointly control those policies.’

“Joint control” is the contractually agreed sharing of control of an arrangement, which exists only when decisions about the relevant activities require the unanimous consent of the parties sharing control.

Section 29A of IBC 2016 talks about the ineligibility criteria for a Resolution Applicant to submit a resolution plan. As per Explanation 1 to Section 29A, Associated Company is included in the definition of the Connected Person. Also, Section 5(24) of the IBC determines an associated company as a related party. It means that the associated company comes under the ambit of both, connected person and related party.

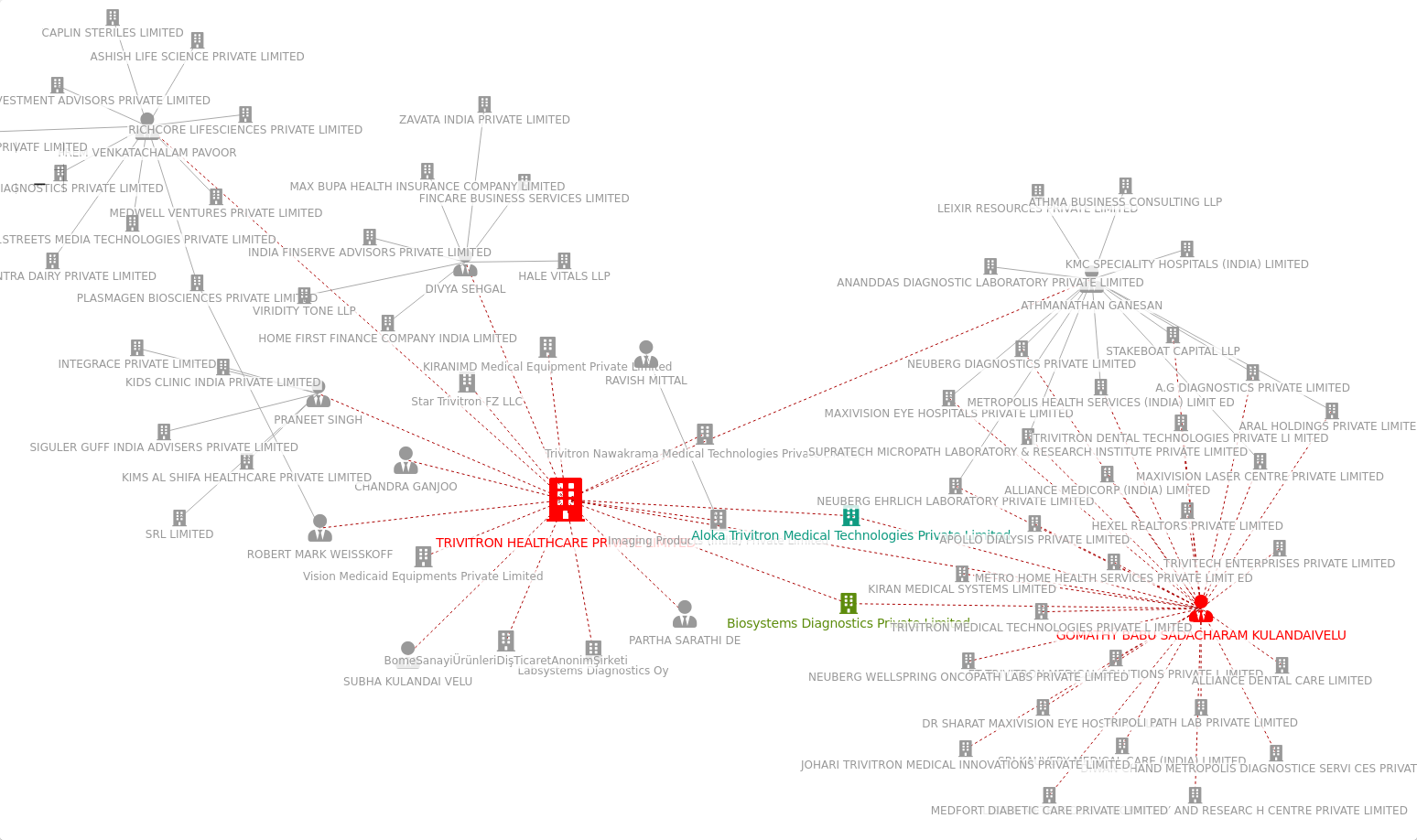

A connected/associated entity discovery as executed on SignalX.ai by an Insolvency Professional.

Section 29A of the IBC 2016 expressly bars Associated Companies from participating in the resolution process. The participation of an associated company gives rise to the possibility that it may influence transactions or settle off its claim preferentially over other creditors. It may enter into transactions with the corporate debtor on favorable terms and conditions creating a biased environment for the creditors.

A thorough analysis of all the key individuals and entities involved in the Corporate Debtor, and ascertaining their independence with key individuals and entities involved in the Resolution Applicant, is crucial to arrive at a defendable qualification of the RA by the Insolvency Professional. With increasingly opaque company structures, and the expansive scope of ‘Connected Parties’ as per the IBC, leveraging technology platforms like SignalX.ai to identify and discover connected parties can drastically reduce the time it takes to research the RA and also reduces the scope for misjudgement on the Resolution Professional’s part.

Non cooperative Debtors can make it further difficult for the Resolution Professional to make robust judgements on RA eligibility. Seemingly small RAs can sometimes have a vast network of connected parties, like the one shown below, which exponentially increases the complexity of ascertaining independence as required by Section 29A of the IBC.

Aside from the Insolvency perspective, independence checks are also of significance when it comes to generating defendable valuation reports. Rule 3(2)a of the Registered Valuer Rules states that “no partnership firm or company shall be eligible to be a registered valuer, if it has been set up for objects other than for rendering professional or financial services, including valuation services, and that in the case of a company, it is a subsidiary, joint venture or associate of another company or body corporate.” The Honorable High Court of Delhi notified the same in Cushman And Wakefield India Private Limited Vs. Union Of India & Anr.

Being an associate company or an associated entity will also entertain considerations under the Companies Act 2013, such as the requirement to be included in the consolidated financial statements and to be flagged as a related party when it comes to transactions etc.

Leveraging technology is increasingly a must for compliance professionals like Registered Valuers and Insolvency Professionals to execute defendable analyses in their projects. SignalX enables hundreds of risk and compliance professionals to execute a wide range of checks and analyses, like ascertaining independence between entities, at scale.